4 things you need to start doing today to have a financially healthy future!

Most of us have been taking care of our health by eating healthy food and working out regularly but how many of us focus on keeping our financial future healthy? Lets look at what we need to start planning and doing today in order to have a better and brighter tomorrow:

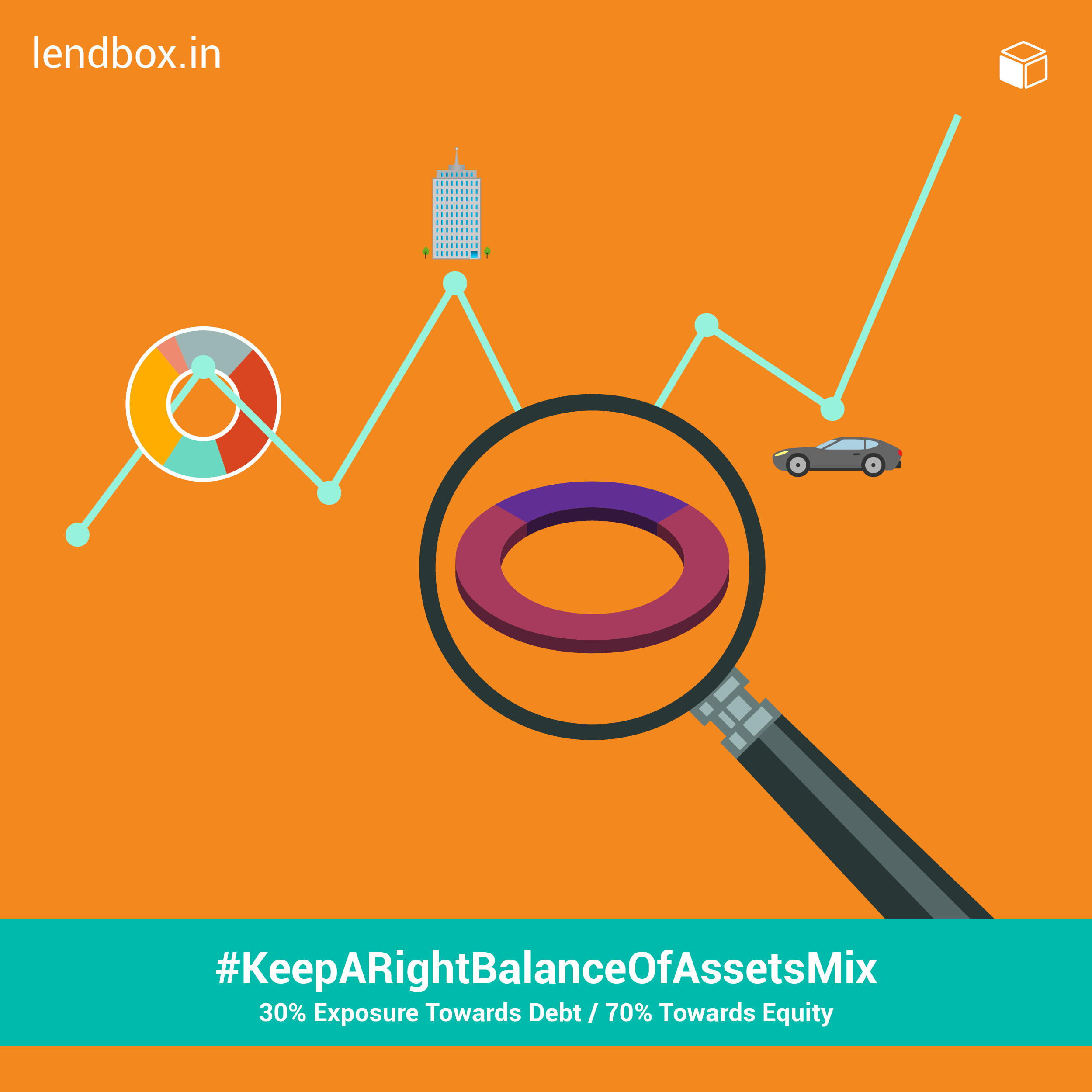

1. Keep a right balance of Assets mix:

Let us understand the difference between debt and equity as an asset class. Plainly, debt is an investment which would give you assured fixed return while on the flip side the return on equity could move in either direction i.e. positive or negative. On the positive side it can inflate your returns almost to the extent of infinity or on the negative side it can erode your invested capital.

Basic thumb rule states that your exposure towards debt should be limited to the percentage of your age and your exposure towards equity should be 100 less your age i.e. if your age is 30 then you should have 30% exposure towards debt / fixed income instruments and the remaining 70% (100-30) towards equity.

This proportion may change based on ones risk appetite and positioning to achieve his/her financial goals. It is possible that as your age increases your ability to take risk decreases and steadily you start achieving your goals in life. If you have a higher risk appetite then the proportion of equity investment to lending will be higher than the standard. The proportion of lending increases as you arrive near your financial goal.

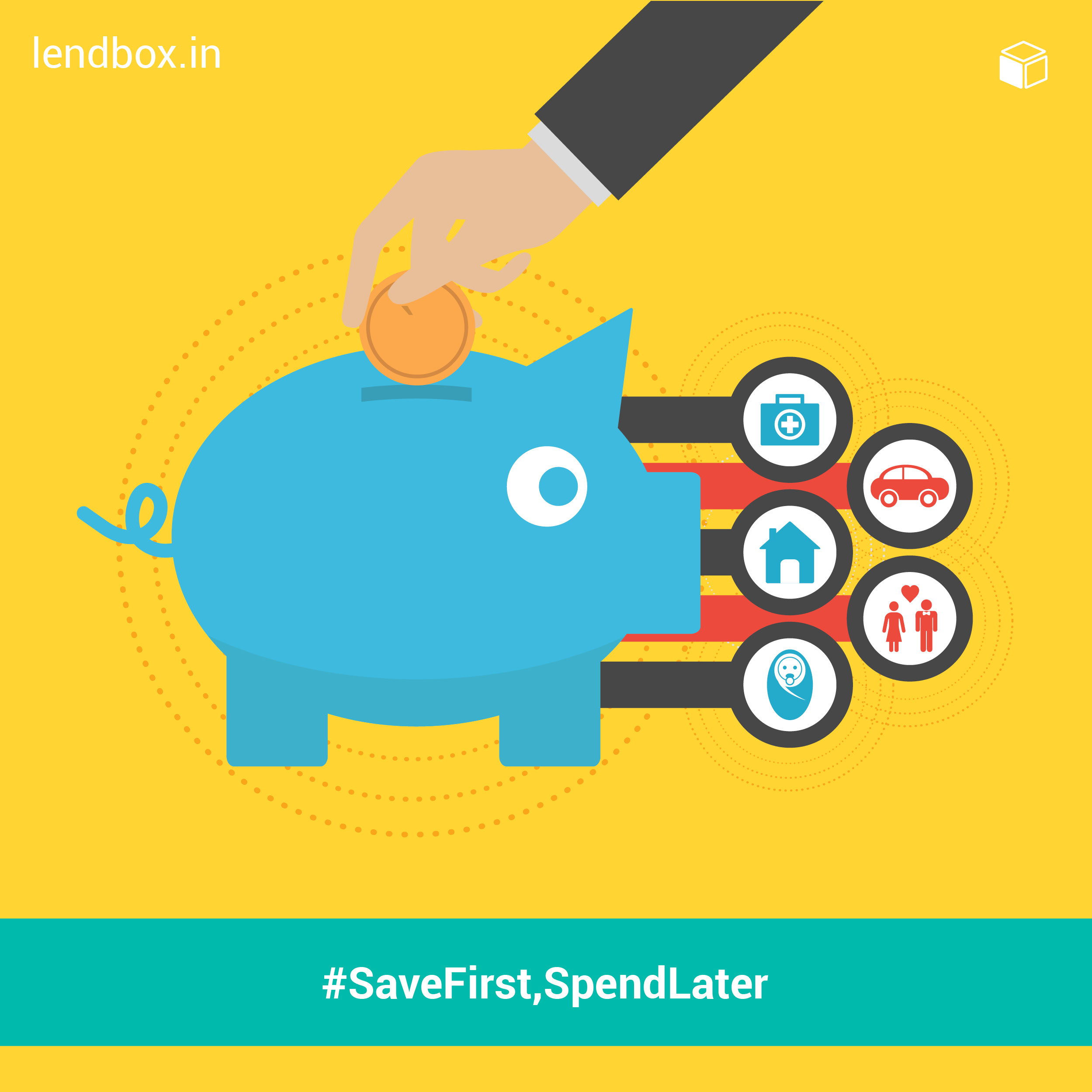

2. Save first, spend later:

Today's young earning population usually claims that they are not earning enough to save. The youth spend a high proportion of their income on expensive gadgets, branded clothes and accessories and usually live on credit. This practice of using the credit card to pay for your regular expenditure - may be because of lack of sufficient income or just to collect reward points should be stopped. Instead one should save the minimal amount - as stated in the 50 - 30 - 20 rule in the article 4 Steps to attain Financial Nirvana and adjust ones expenditures to accommodate the savings. As per the rule, your savings should be at least 20% of your regular income. This saving could be utilized for achieving one of your financial goals in life or could be put to use during emergency.

3. List your financial goals:

Every individual has some basic goals in life such as children's higher education and marriage, purchase of a house property, annual vacation, retirement planning etc. He / She should clearly state the number of years in which they wish to achieve them and the cost of doing so. With these three data points you could calculate the then value of achieving the goal based on assumed cost of inflation.

Let us understand this with the help of an example: You are 35 years old and you plan to collect Rs. 5 crores at present price for your retirement 25 years hence i.e. at the age of 60 years. Assuming that the cost of living index i.e. the inflation during the same period is expected to be 7% p.a., the amount that you should have collected when you reach 60 would be Rs. 27 crore [Rs. 5 cr x (1+7%)^25years]. Similarly you will have to pen down all the present value (PV), the time frame in which you aim to achieve it in for all your other goals. With assumed inflation figures, you could arrive at the future value (FV) of your goal.

4. Develop a strategy to achieve the goals:

It's not only important to list down your goals in life but also equally important to build a savings and investments based strategy to reach it. Based on your risk appetite, one has to check if it's possible to attain it in the desired extent and the time; if not then one has to adjust the amount / time accordingly. You could be required to cut down your expenditure on comforts and luxury to achieve it.

Let us say that you require Rs. 25 lakhs at present value after 5 years for your Childs higher education. Assuming education inflation to be 10% p.a. the then value / future value of this goal will be Rs. 40 lakhs. With your present level of income, expenditure, savings and investments you are falling short of a few lakhs to achieve your goal. In such a case you could either increase the tenure in which you could achieve the goal or decrease the value of the goal. If you wish to do neither one of them then you could cut your expenditure on vacation, purchase of electronic gadgets etc. or take up an extra job to earn more income, hence save and invest further for your goal or invest in riskier assets in contrast to your risk appetite. This adjustment of income, expenditure, risk appetite, tenure and / or value of the goal is a part of strategy building.